On The Efficiency Of Betting Markets

26th May 2026

A common misconception about profitable betting is that it requires consistently outsmarting the market. In reality, the market prices events correctly on average. Profitable algorithms do not bet on every opportunity they see — they bet on almost none of them.

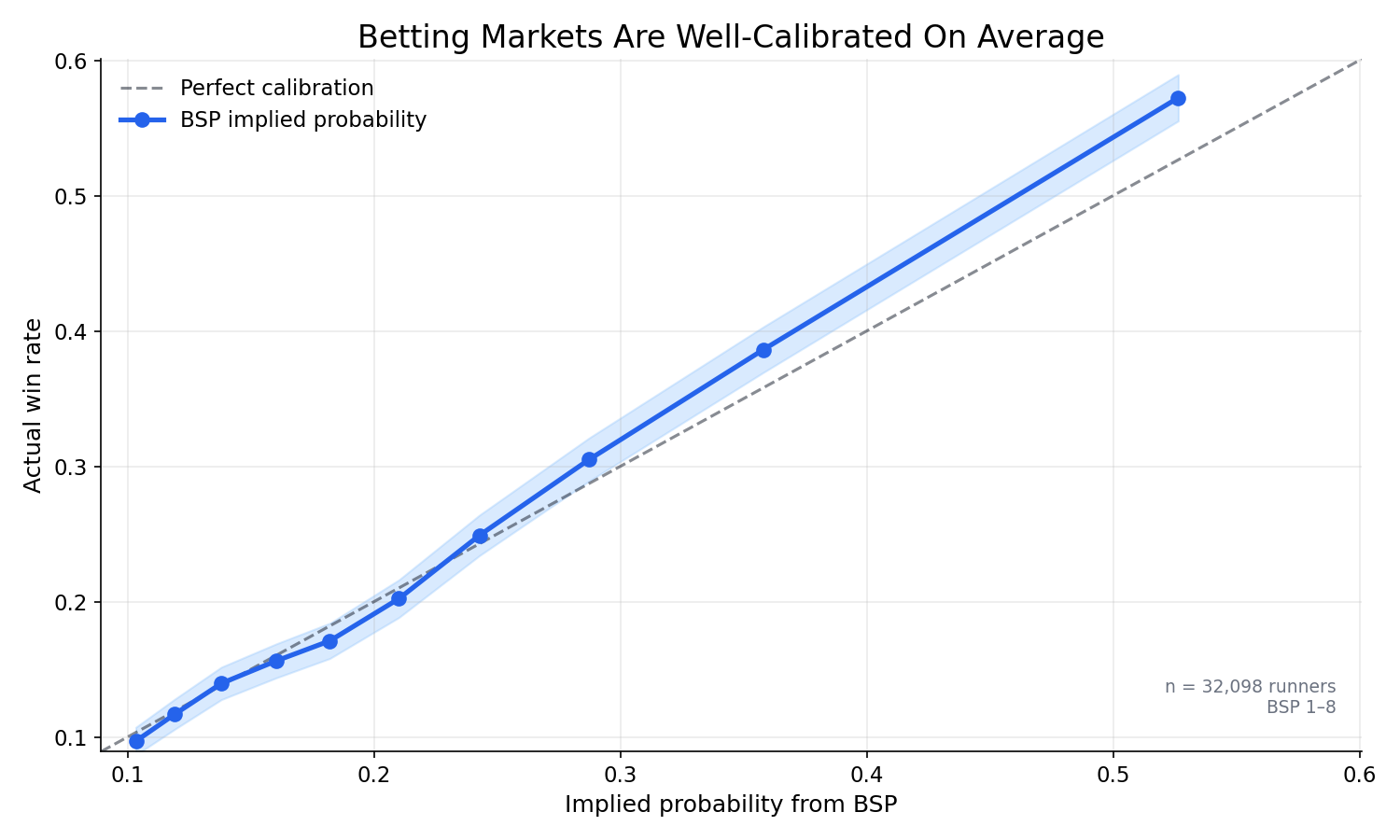

The Market Is Well Calibrated

Betting markets behave like financial markets. Sharp money from syndicates, professionals, and algorithms continuously corrects mispricings. The result is that the implied probability from the odds:

tracks the true win probability closely across the board. The chart below shows this for a liquid exchange market in 2026 — when BSP implies a 20% chance, selections win roughly 20% of the time.

This is why betting randomly loses money. The edge from any single bet is approximately zero before the exchange commission, and negative after it.

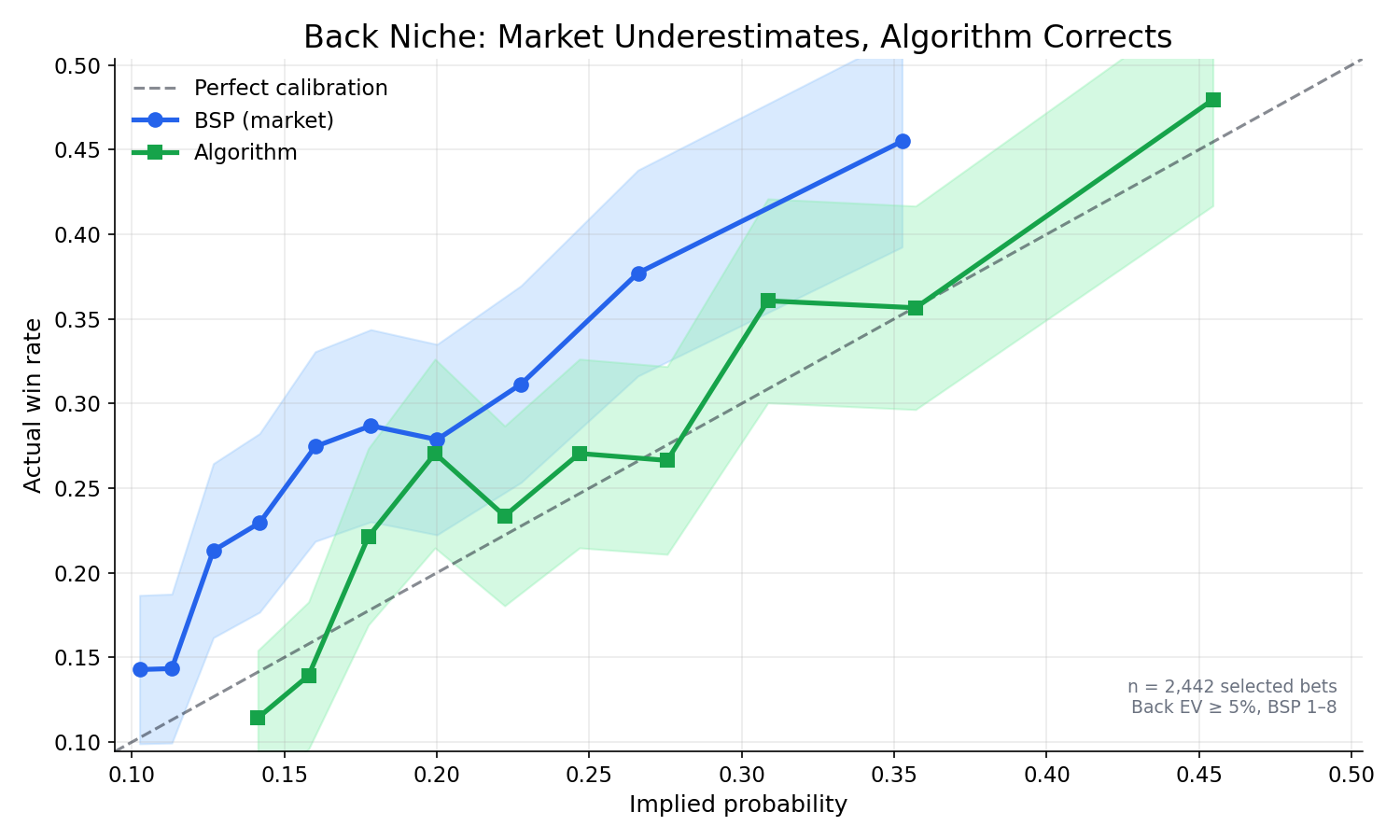

Algorithms Find Where The Market Is Wrong

The market is calibrated on average — but not everywhere. A model trained on a specific niche can find systematic gaps where the market consistently misprices a subset of runners.

For back bets, this means finding runners the market undervalues: BSP implies a lower win probability than actually occurs. The chart below shows this for bets filtered to back EV ≥ 5% at BSP 1–8. The blue line (BSP) sits above the diagonal — runners win more often than BSP predicts. The algorithm's calibration (green) tracks the diagonal closely.

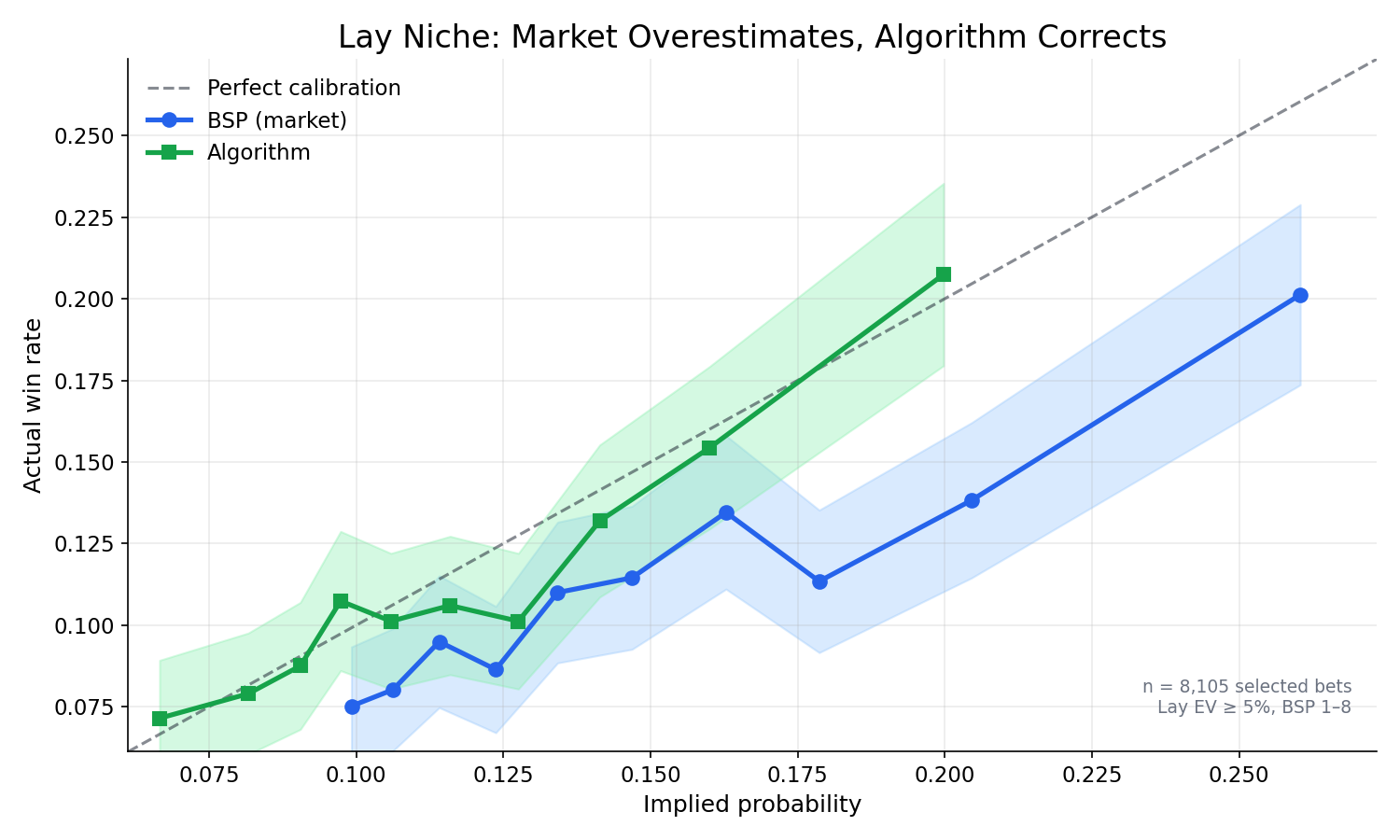

The same logic applies in reverse for lay bets. Here the algorithm identifies runners the market overvalues — BSP implies a higher win probability than actually occurs — making it profitable to take the other side.

Selectivity Is The Strategy

The edge does not come from finding better markets — it comes from filtering the same markets more accurately. An algorithm that bets on everything converges to the market average, which is negative after commission. An algorithm that only bets when its estimated edge exceeds a threshold:

selects from the positive tail of the edge distribution. Most opportunities are passed on. That silence is intentional.

Scaling With Kelly

Once a genuine edge is identified, the Kelly criterion determines how much to stake:

where is the expected return on stake. The stake scales linearly with edge — a 4% edge gets twice the stake of a 2% edge, and a zero-edge bet gets nothing. A moderate edge, applied consistently at correct sizing, compounds meaningfully over time.

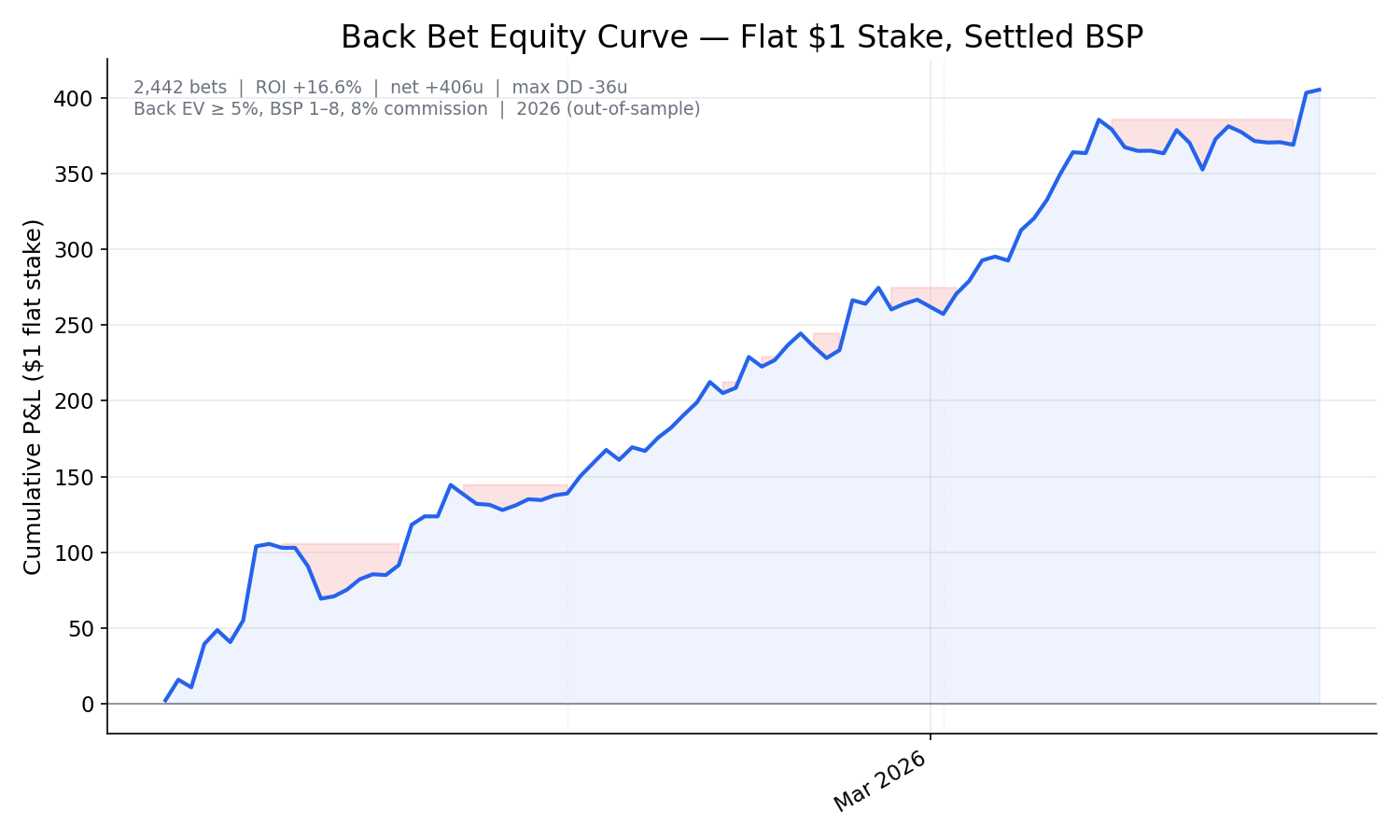

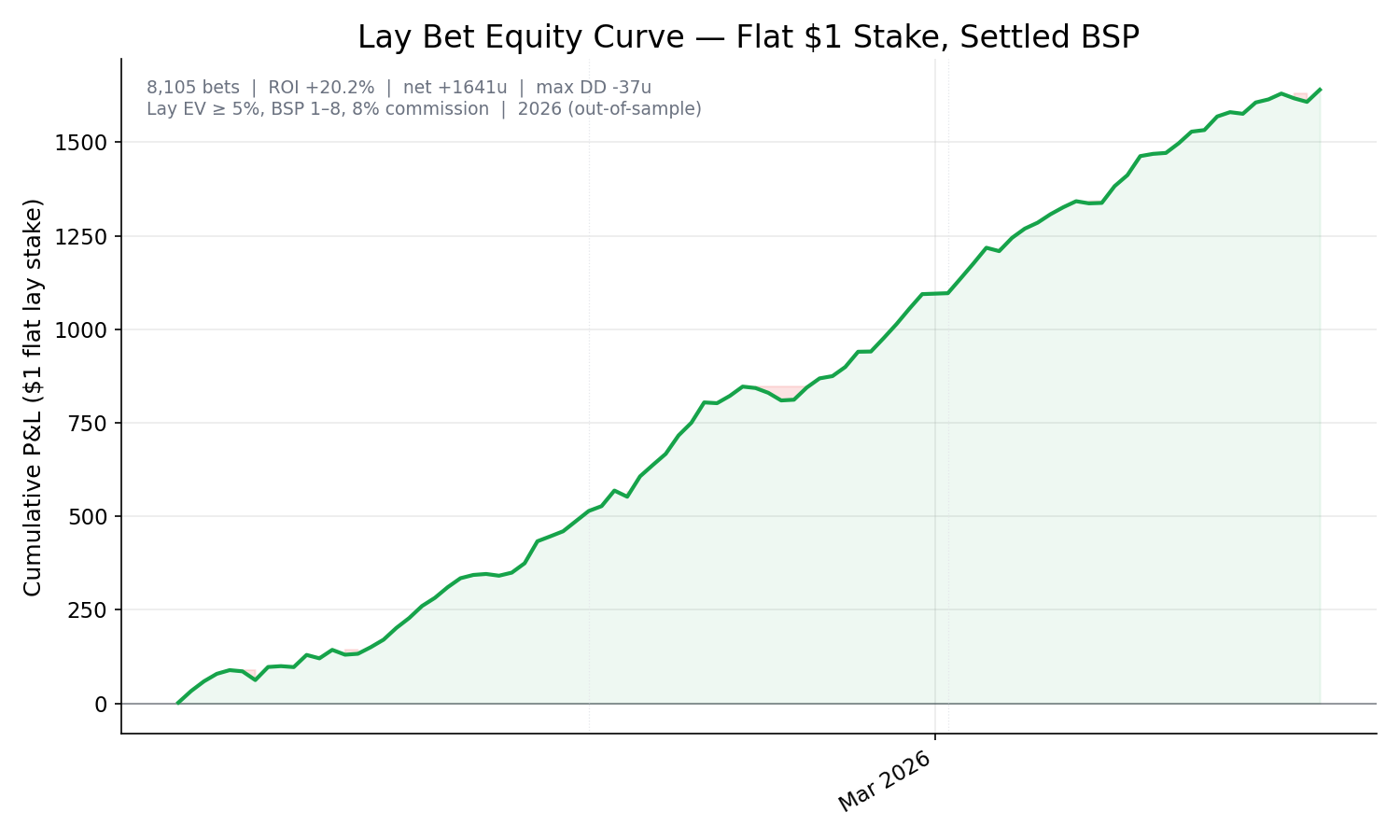

Real Results

The following equity curves show flat $1 stake performance on 2026 out-of-sample data, settled at BSP with 8% commission. The model was trained on 2023 data only.

Both strategies are profitable at around 17–20% ROI on turnover from a relatively modest edge. The back curve is noisier — fewer bets at higher odds — while the lay curve is smoother because the win rate is high and individual losses are bounded by the BSP cap of 8.

The market is approximately right on average. Making money means finding the narrow set of moments when it is not, and doing nothing the rest of the time.